Answer:

The correct answer is option (A) $2,600

Explanation:

Given data;

The data given can be tabulated below for easy understanding

Pairs Flow Distance Flow distance

X-y 30 20 600

Y-Z 280 10 2800

Z-X 180 10 1800

Total flow = 600 +2800 + 1800 = 5200

To calculate the total weekly cost, we use the formula;

Total weekly cost is = Total flow * Cost of per load

= 5200 *0.5

$2,600

Answer:

b,

Explanation:

treatment of hazardous waste is preferred to the other options, in a sense they all have side effect. But if waste are treated it reduces the rate of pollution.

Answer:

the transaction record as given below

Explanation:

given data

sold merchandise = $3,200

terms n/30

sales tax percentage = 6%

solution

as here with 6% sale tax payable is

sale tax payable = 6% of 3,200 = $192

and account Receivable will be $192 + $3200 = $3392

so

we get here the transaction record that is as

date title Dr. Cr.

25-Mar Accounts Receivable 3392

Sale 3200

Sales tax payable 192

25-Mar Cost of goods sold

Inventory

Answer:

Mark-up = 101.9%

Explanation:

<em>Mark up is the percentage of the product cost that is made as profit. It is profit expressed as a percentage of the product cost.</em>

Mark-up = profit/product cost × 100

Mark-up = $55/54 × 100 =101.85%

Mark-up = 101.9%

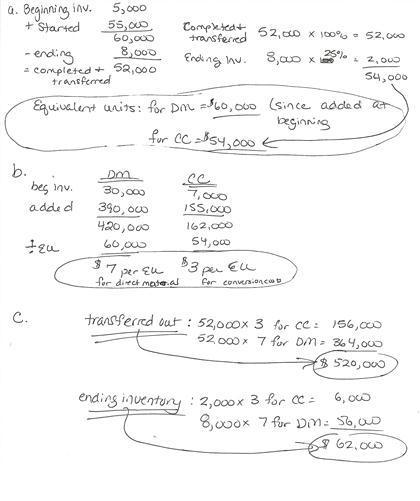

Answer:

Answer for the question is given in the attachment.

Explanation: