Answer:

Ending inventory cost= $1,494

Explanation:

Giving the following information:

Beginning Inventory: 300 $780

Purchases:

May 10: 400 units for $1,170

June 15: 500 units for $1,260 ($2.52 per unit)

August 28: 300 units for $990 ($3.3 per unit)

The company had 500 units were in its ending inventory at the end of the year.

Under FIFO (first-in, first-out), the ending inventory cost is calculated using the cost of the last units incorporated.

Ending inventory cost= 300*3.3 + 200*2.52= $1,494

Answer:

The answers are:

<u>January 10</u>

Cash $816,000

Common stock $510,000

Contributed capital in excess

of par value, common stock $306,000

<u>January 15</u>

Equipment $80,000

Common stock $50,000

Contributed capital in excess

of par value, common stock $30,000

<u>February 1</u>

Organizational expenses $3,000

Common stock $25,000

Contributed capital in excess

of par value, common stock $500

Explanation:

Contributed capital in excess of par value is the amount of money (or other assets) over the par value of stock (in this case $5 per common stock) that the company received form shareholders in exchange for stock.

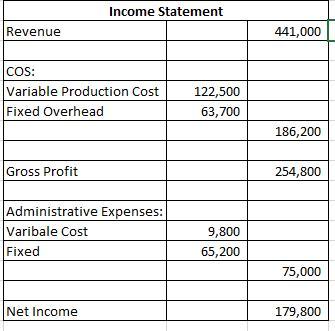

Answer:

Refer To The attached screen shot. It contains the Income Statement Prepared under Absorption Costing.

Explanation:

Absorption Costing assumes that the Manufacturing Costs include Direct Material, Direct Labor, Variable Overhead, and Fixed Overhead. Whereas, Selling and Administrative Expenses are classified as period Costs. These period costs are recognized in the period in which they are incurred. On the other hand, the manufacturing costs are recognized when the goods on which the costs were incurred are sold. That's why we don't recognize $78,000 as a Fixed Overhead because these overhead costs were incurred to produce 6,000 rackets. We have to calculate the fixed overhead cost per unit and multiply it with the units sold.

I hope I made it clear. If you have any queries, feel free to contact me.

Thanks.

The holder of a promotional permit may MAY ENGAGE IN ACTIVITIES TO PROMOTE AND ENHANCE THE SALE OF ALCOHOLIC BEVERAGES ON BEHALF OF THE ALCOHOL MANUFACTURERS. The permit licensed the holder to market alcohol drinks without any consequence attached but he must be qualified to get the licence and he is also expected to pay annual fees.

The cost of goods sold for the year is $500.

Since FIFO method is to be used, the cost of goods sold for the year should be the cost of its first purchase regardless of when the product is actually bought. Thus, the cost of goods sold for the year is $500 ($500 × 1).