Answer:

See explanation section

Explanation:

Requirement A - Specific Identification

Ending inventory are the inventory that are not sold during the period.

Beginning Inventory remain unsold = 15 Units × $6.00 = $90.00

January 20 inventory remain unsold = 5 units × $5.00 = $25.00

<u>January 30 inventory remain unsold = 180 units × $4.50 = $810 </u>

<em>Total Ending Inventory = 200 units = $925.00</em>

Cost of goods sold are the cost of the product sales during the period.

Beginning Inventory sold = 125 units × $6.00 = $750.00

<u>January 20 inventory sold = 55 units × $5.00 = $275.00</u>

<em>Cost of goods sold = 180 units = $1,025.00</em>

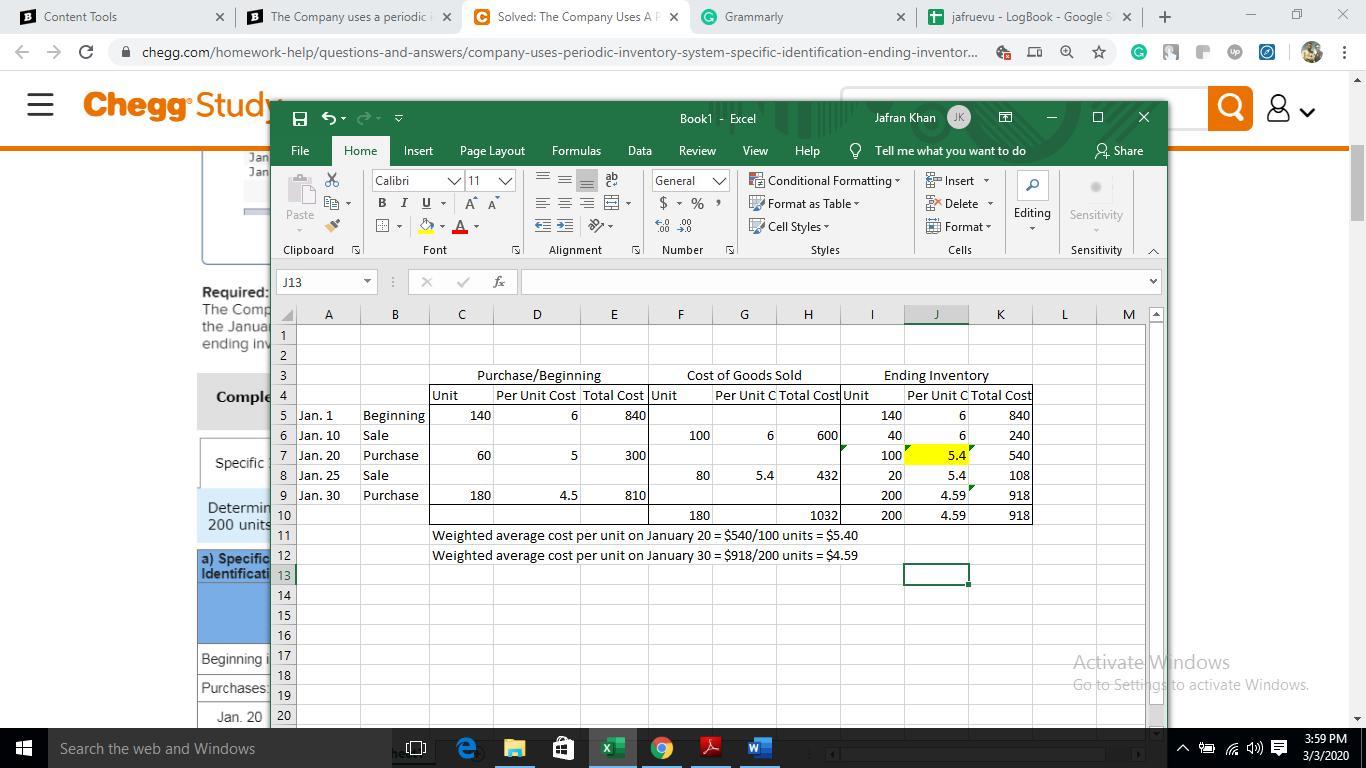

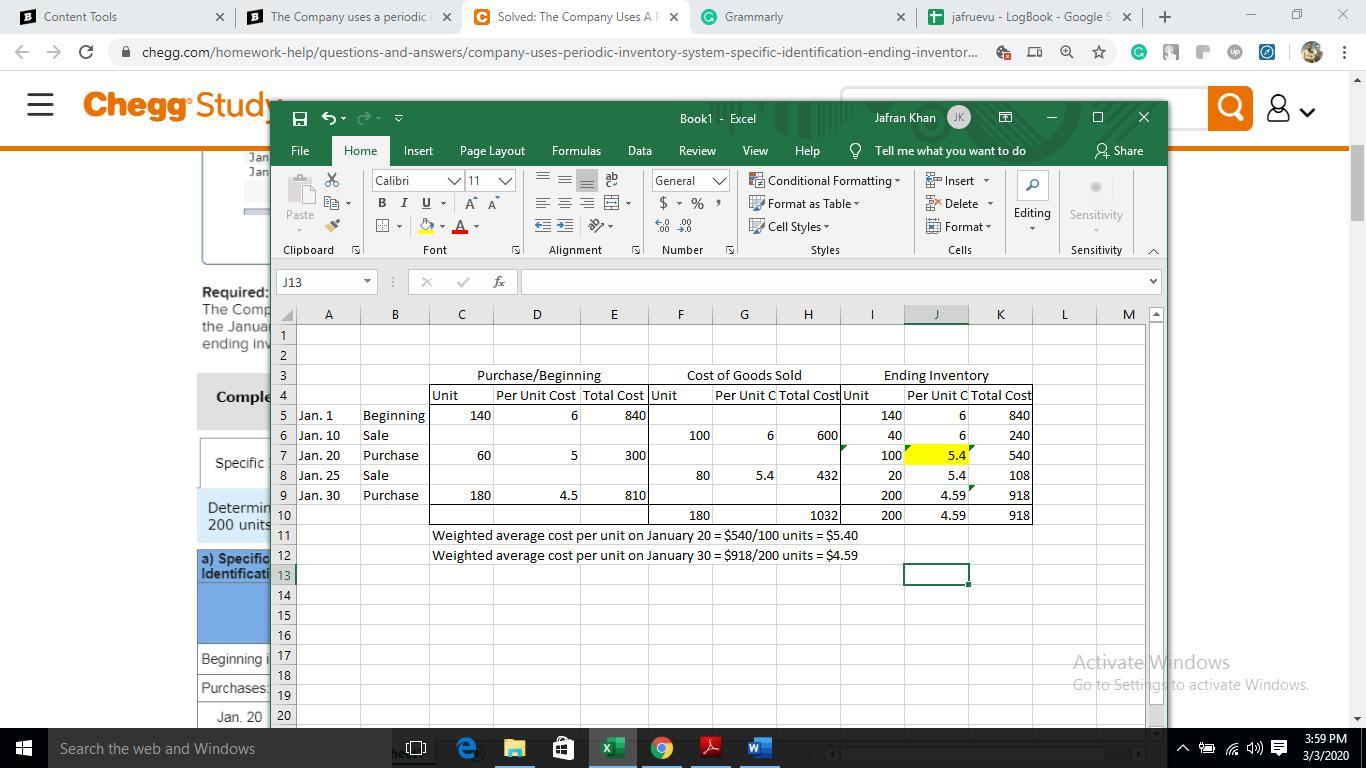

Requirement B - Weighted Average

Ending inventory

<u>See the below image:</u>

Cost of goods sold

Beginning Inventory sold = 100 units × $6.00 = $600.00

<u>January 20 inventory sold = 80 units × $5.40* = $432.00</u>

<em>Cost of goods sold = 180 units = $1,032.00</em>

* - See the image below to get the appropriate answer

Requirement C - FIFO

Ending inventory

Beginning Inventory remain unsold = 0 Units × $6.00 = $0.00

January 20 inventory remain unsold = 20 units × $5.00 = $100.00

<u>January 30 inventory remain unsold = 180 units × $4.50 = $810.00 </u>

<em>Total Ending Inventory = 200 units = $910.00</em>

Cost of goods sold

Beginning Inventory sold = 140 units × $6.00 = $840.00

<u>January 20 inventory sold = 40 units × $5.00 = $200.00</u>

<em>Cost of goods sold = 180 units = $1,040.00</em>

Requirement D - LIFO

Ending inventory

Beginning Inventory remain unsold = 140 Units × $6.00 = $840.00

<u>January 20 inventory remain unsold = 60 units × $5.00 = $300.00</u>

<em>Total Ending Inventory = 200 units = $1,140.00</em>

Cost of goods sold

<u>January 30 inventory sold = 180 units × $4.50 = $810.00</u>

<em>Cost of goods sold = 180 units = $810.00</em>