Answer:

The correct answer is letter "C": weak competitors in the industry.

Explanation:

Organizational resources are all those assets a company has that allows the firm to maintain or improve its production process. Organizations can have <em>human, capital, monetary, </em>and <em>raw materials resources</em>. After properly combined, the firm's resources created final goods.

In that case, competitors do not represent assets firms can use in their production process.

Answer:

1.Since there is spare capacity in the consumer division, the acceptable transfer prices are variable cost per unit - market price per unit

i.e. $104-$150

The transfer price should be set in between the two. However, $150 is an appropriate price

2. Income will increase as follows:

Consumer Division = (115-104)*2880 = $31,680

Commercial Division = (150-115)*2880 = $100,800

Company = $132,480

3) check the attached file

4.Income will increase as follows:

Consumer Division = (126-104)*2880 = $63,360

Commercial Division = (150-126)*2880 = $69,120

Company = $132,480

Explanation:

check attached files for explanation well detailed.

Answer:

<u>Monopolist competition</u>.

Explanation:

The market structure of monopolistic competition occurs when there are several companies offering similar products, which even though substitute products cannot be considered perfect substitutes. Monopolistic competition is characterized when in the market there are many sellers competing for a higher market position of some product or sector. This type of monopolistic competition is characterized by free entry to other companies, which makes it increasingly competitive in the pursuit of customer preference.

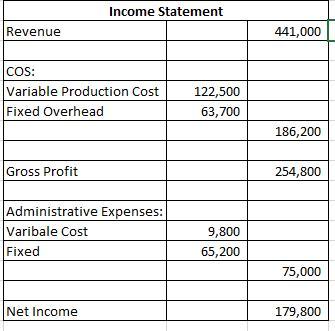

Answer:

Refer To The attached screen shot. It contains the Income Statement Prepared under Absorption Costing.

Explanation:

Absorption Costing assumes that the Manufacturing Costs include Direct Material, Direct Labor, Variable Overhead, and Fixed Overhead. Whereas, Selling and Administrative Expenses are classified as period Costs. These period costs are recognized in the period in which they are incurred. On the other hand, the manufacturing costs are recognized when the goods on which the costs were incurred are sold. That's why we don't recognize $78,000 as a Fixed Overhead because these overhead costs were incurred to produce 6,000 rackets. We have to calculate the fixed overhead cost per unit and multiply it with the units sold.

I hope I made it clear. If you have any queries, feel free to contact me.

Thanks.