Answer:

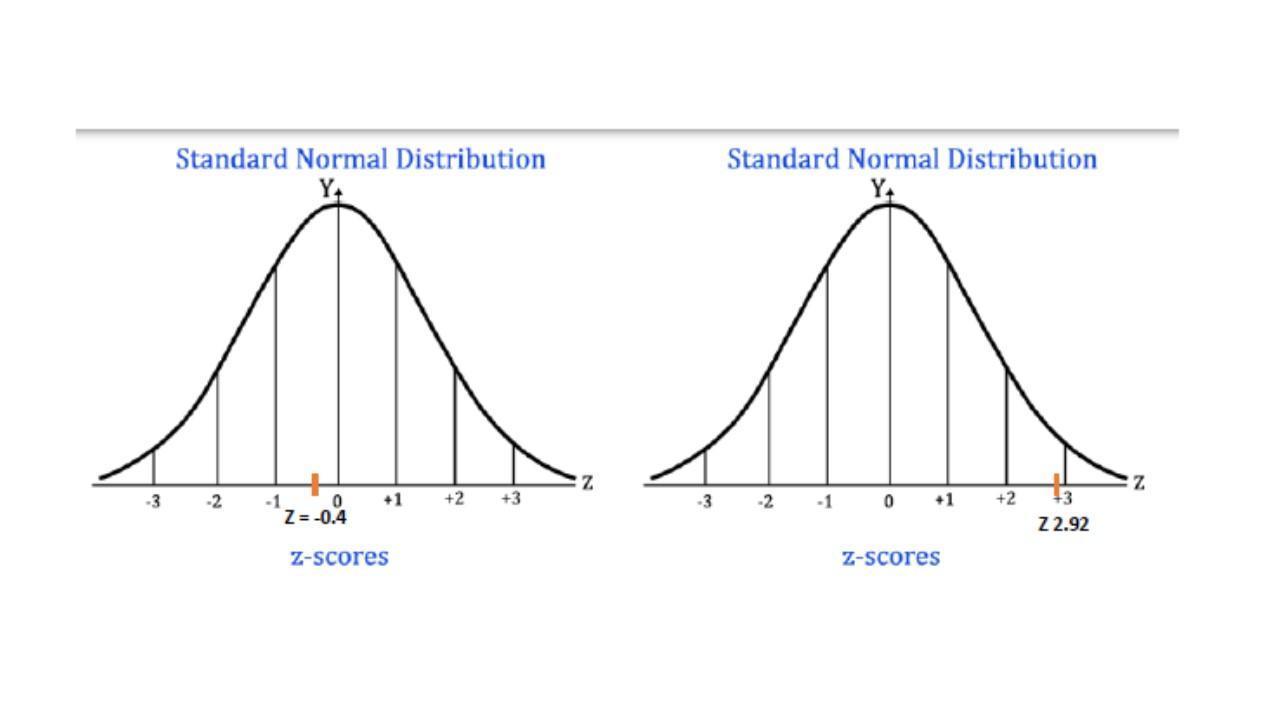

- a) For net sales: Z = - 0.4

For number of employees: Z = 2.92

- b) Lacation of the two Z values: see the pitcture attached

- c) - Clarion's sales are less than the average sales of other fabricators

- Clarion's number of employess is greater than the average number of employees of the other fabricators.

Explanation:

For the net sales, the mean is $180 million and the standard deviation is $25 million.

For the number of employees, the mean is 1,500 and the standard deviation is 120.

Clarion Fabricators had sales of $170 million and 1,850 employees.

<u><em>a. Convert Clarion’s sales and number of employees to z values. </em></u>

The Z-value or Z-score of a normal variable is the normalized mean. It tells how many standard deviations a value is away from the mean.

The formula to calculate the Z-value is

Where:

- x is the value of the variable

- μ is the mean

- σ is the standard deviation

For the net sales:

For number of employees:

<u><em>b. Locate the two z values. </em></u>

The graph of the standardized normal distribution is a bell-shape curve, with the Z=0 value as the axis of symmetry, this is the central value. The negative values are to the left of the axis of symmetry and the positive vaule are to the right of the axis of symmetry.

Thus, Z = - 0.4 is to the left of Z = 0, and Z = 2.96 is to the right.

I have attached a figure with both Z-values located. Look at the attached pitcures.

<u><em>c. Compare Clarion’s sales and number of employees with those of the other fabricators</em></u>

Since the Z-value for the net sales is negative (-0.4), the net sales of Clarion are less than the average sales of the other fabricators. If you look at the cummulative distribution in a table, z = - 0.4 means that 34.46% of the other fabricators have lower net sales.

Since the Z-value for the number of empolyees is positive (2.92), the number of employees of Clarion is greater than the average number of employees of the other fabricators. Looking at a table of cummulative probabilityz = 2.92 means that 99.83% of the fabricators have less employees than Clarion.