Yes. It will only affect the asset portion of the company's balance sheet.

When the company buys the one-year insurance policy, the journal entries will be:

Debit Credit

Prepaid insurance 1,000

Cash 1,000

When the insurance expires after a year, the journal entries will be:

Insurance Expense 1,000

Prepaid Insurance 1,000

Note:

Prepaid Insurance and Cash are both found in the assets section of the balance sheet.

Insurance Expense is found in the Income statement of the company and not in the balance sheet.

Answer:

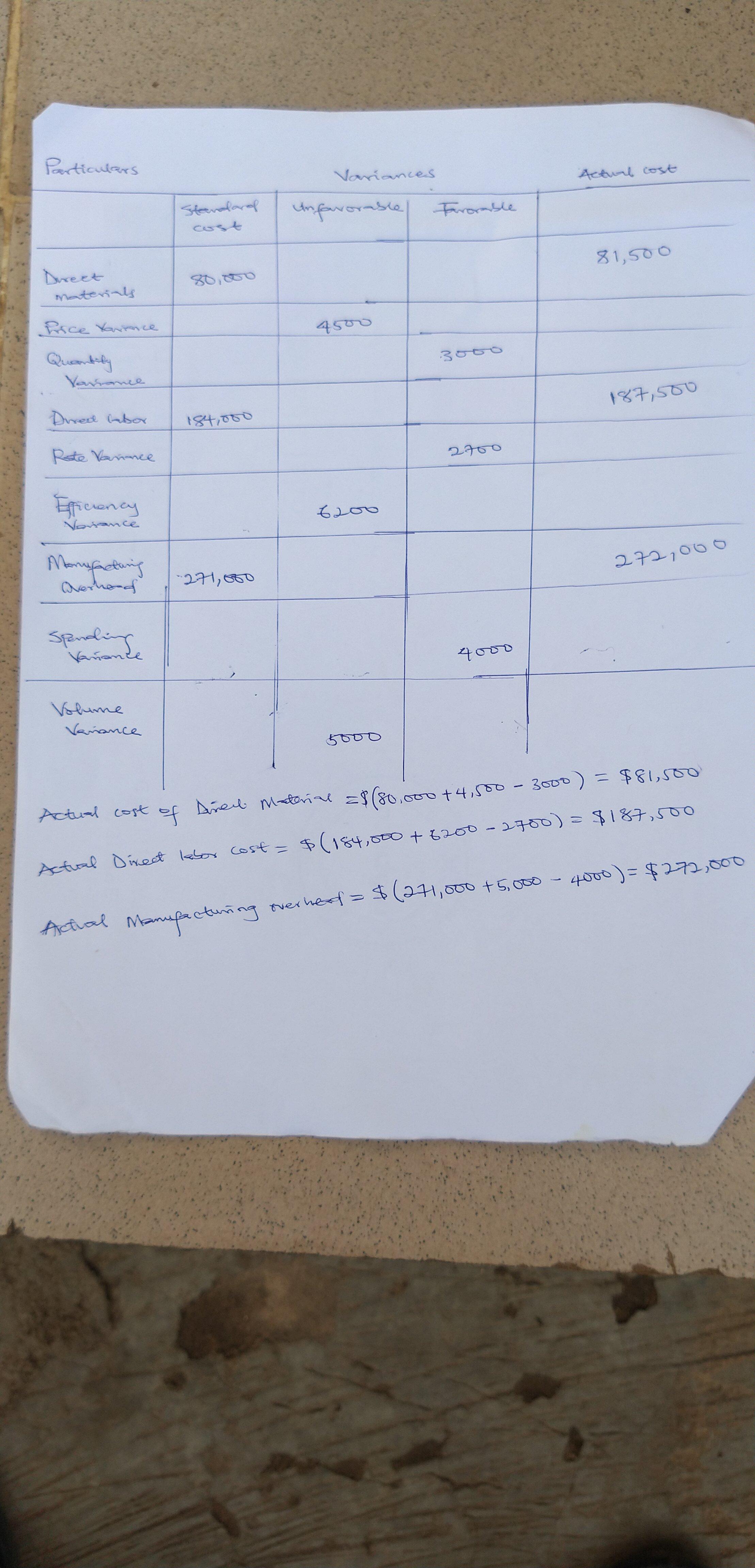

Actual Direct material cost = $81,500

Actual Direct labor cost = $187,500

Actual manufacturing overhead = $272,000

Explanation: kindly see attached picture for detailed explanation.

Variances ; Standard Cost Unfavorable Favorable Direct materials $ 80,000 Price variance $ 4,500 Quantity variance $ 3,000 Direct labor 184,000 Rate variance 2,700 Efficiency variance 6,200 Manufacturing overhead 271,000 Spending variance 4,000 Volume variance 5,000 Determine the actual costs incurred during the month of May for direct materials, direct labor, and manufacturing overhead.

Connie's next step should be

Not - go back and revisit her plan objectives

Maybe - Conduct primary research and analyze Fred's current customers.

<h3><u>

Explanation:</u></h3>

It is very essential for an entrepreneur who decides to start a new business to have a business plan that helps him in setting up the businesses in the right track and usage of funds in an effective manner. A business plan acts as a blue print of a new business and the objectives and resource utilization.

In the scenario give, Fred decides to start a new boutique and has conducted researches geographic locations and the type of boutiques supported by the demography. She must not then go back and review her plan objectives as she has decided to start it with a good plan and she may conduct a primary research about the current customers of him.

Answer:

It is more profitable to continue processing.

Explanation:

Giving the following information:

A company has inventory that cost $50,000. Its scrap value is $65,000. The inventory could be sold for $150,000 if manufactured further at an additional cost of $80,000.

Sell for scrap= 65,000 - 50,000= 15,000

Continue processing= 150,000 - 80,000 - 50,000= 20,000