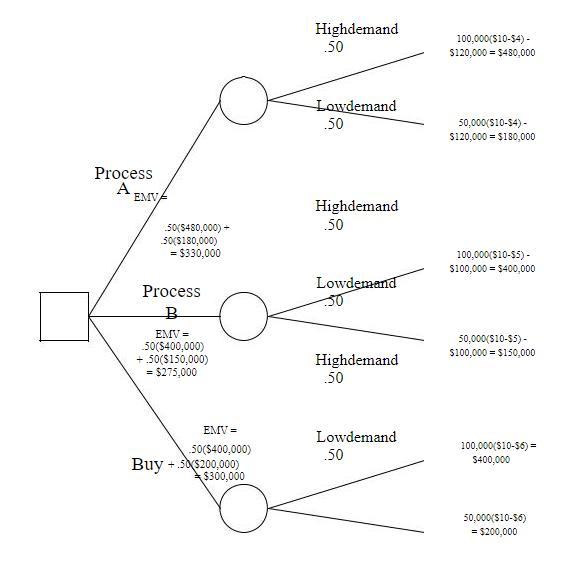

Answer:

The best choice is process A since it has the highest EMV of $330000

Explanation:

there is a 50% chance that they will sell 50,000 units, and a 50% chance that they will sell 100,000 units

The decision tree is attached below, the calculations for the decision tree is given as:

The item sells for $10. Process A requires an investment of $120,000 for design and equipment, but results in a $4 per unit cost.

If there is high demand, they will sell 100,000 units, The profit = 100000($10-$4) - $120000 = $480000.

If there is low demand, they will sell 50,000 units, The profit = 50000($10-$4) - $120000 = $180000.

The EMV of process A = 0.5($480000) + 0.5($180000) = $330000

Process B requires only a $100,000 investment, but its per unit cost is $5

If there is high demand, they will sell 100,000 units, The profit = 100000($10-$5) - $100000 = $400000.

If there is low demand, they will sell 50,000 units, The profit = 50000($10-$5) - $100000 = $150000.

The EMV of process B = 0.5($400000) + 0.5($150000) = $275000

If the item is outsourced, there is virtually no cost other than the $6 per unit that they would pay their supplier

If there is high demand, they will sell 100,000 units, The profit = 100000($10-$6) = $400000.

If there is low demand, they will sell 50,000 units, The profit = 50000($10-$6) = $200000.

The EMV of Buying = 0.5($400000) + 0.5($200000) = $300000

The best choice is process A since it has the highest EMV