Answer:

required purchase 83,500

Explanation:

The cost of inventory in july sales and our desired ending invenory is the amount we need. the beginning inventory is a portion of this demand already fullfil, we need to purchase for the difference.

cost of inventory sales for July:

70,000 x (1 - 45%) = 38,500

desired ending inventory 105,000

beginning inventory <u> (60,000) </u>

required purchase 83,500

Answer:

Anticipatory repudiation.

Explanation:

Penelope's attitude or follow up towards her ordeal above is an example of anticipatory repudiation.

This is also termed an anticipatory breach, is a term in the law of contracts that describes a declaration by the promising party to a contract, that he or she does not intend to live up to his or her obligations under the contract.

It generally is a breach that constitutes material of contracts that discharge the promisee from all the obligations that they are under.

Itoccurs when the promisor indicates before the time for his performance that he is unwilling or unable to carry out of the contract.

When the employees are inefficient the manager should take proper steps to improve the performance.

Explanation:

When Mohamed is seeing that his employees are not working properly ,he should take proper steps to uplift the performance that is, the manager should pay attention on the employee when they are facing problems,the managers should give clear feedback, the manager should understand the needs of the employees, the manager should provide proper technology as well as awards should be granted for better performance.

If these things Mohamed keep in mind then he will surely be able to deal with the situation.

Sell the asset, which will drive down the price and cause the expected return to reach the level of the required return.

Answer:

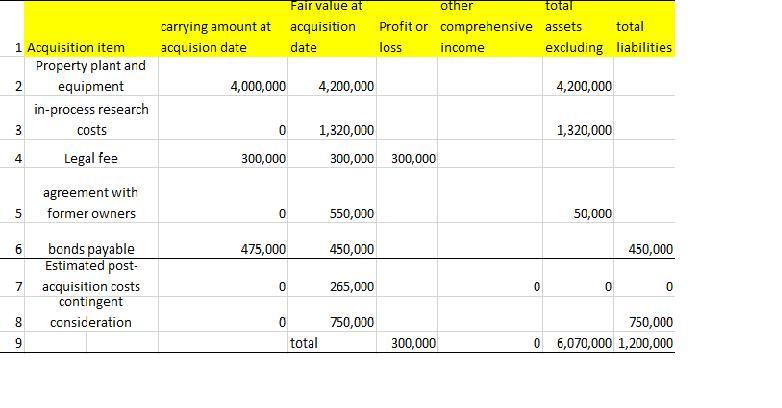

See the attached file below.

Explanation:

There's not much difference between IFRS and U.S. GAAP when it comes to business acquisition.

In accordance with IFRS, FB Corp. would do the following procedure:

(1) record the acquired assets and liabilities at fair value

(2) expense any acquisition related costs such as legal fees

(3) ignore post acquisition costs when determining the values at acquisition

(4) calculate goodwill as the difference between the net assets and the acquisition price less legal fees.