Answer: Bank B is the better investment. In 10 years, her $2,000 will grow to $4,317.85, and with bank A, her $2,000 will grow to $3,700.

Explanation:

Bank A was offering 8.5% simple interest. $2000 with 8.5% simple interest. = A = P(1 + rt)

A = 2000(1+(0.085*10))

= 2000(1+0.85)

= 2000(1.85)

= 3,700

Bank B was offering 8% compounded annually

= A = P(1+r/n)^nt

A= 2000(1+8%/1)^1*10

A= 2000(1+0.08)^10

A= 2000(1.08)^10

A= 2000*2.1589

= 4,317.85

Answer:

See the attached file below.

Explanation:

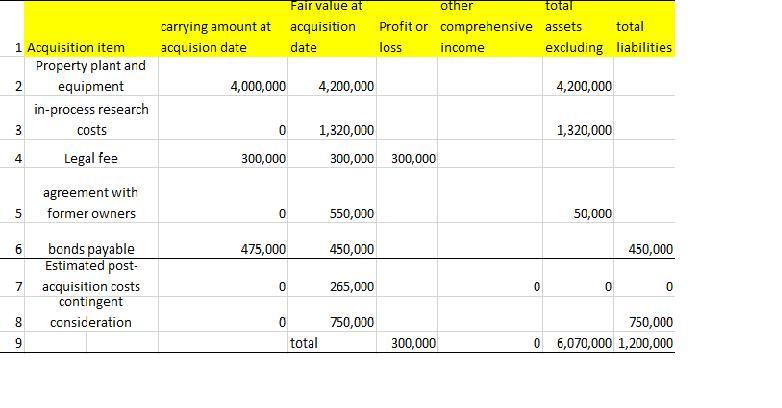

There's not much difference between IFRS and U.S. GAAP when it comes to business acquisition.

In accordance with IFRS, FB Corp. would do the following procedure:

(1) record the acquired assets and liabilities at fair value

(2) expense any acquisition related costs such as legal fees

(3) ignore post acquisition costs when determining the values at acquisition

(4) calculate goodwill as the difference between the net assets and the acquisition price less legal fees.

Answer:

P0 = $51.9956 rounded off to $52.00

Explanation:

The two stage growth model of DDM will be used to calculate the price of a stock whose dividends are expected to grow over time with two different growth rates. The DDM values a stock based on the present value of the expected future dividends from the stock.

The formula for price of the stock today under this model is,

P0 = D0 * (1+g1) / (1+r) + D0 * (1+g1)^2 / (1+r)^2 + ... + D0 * (1+g1)^n / (1+r)^n + [ (D0 * (1+g1)^n * (1+g2) / (r - g2)) / (1+r)^n ]

Where,

- D0 is the dividend today or most recently paid dividend

- g1 is the initial growth rate which is 20%

- g2 is the constant growth rate which is 8%

- r is the required rate of return

P0 = 2.5 * (1+0.2) / (1+0.15) + 2.5 * (1+0.2)^2 / (1+0.15)^2 +

2.5 * (1+0.2)^3 / (1+0.15)^3 +

[(2.5 * (1+0.2)^3 * (1+0.08) / (0.15 - 0.08) / (1+0.15)^3)

P0 = $51.9956 rounded off to $52.00

Answer:

$470,425

Explanation:

The computation of the amount reported as bond payable is shown below:

<u>Particulars Interest at 4.5% Interest at 5% Amortized UnAmortized CV</u>

<u> discount discount </u>

Starting value $30,500 $469,500

($500,000 - $469,500)

June 30 $22,500 $23,475 $975 $29,525 $470,425

($500,000 × 4.5%) ($469500 × 5%)

The six months rate would be the half of the rates given in the question

Answer:

Debit Cash $20,000

Credit M. Alice capital $20,000

Explanation:

We recognize the admission of new partner by debiting the cash that the partnership received in the amount of $20,000 and then record the interest of the new partner by crediting her capital, M. Alice, capital $20,000. Basically, the old partners will agree as to what amount of interest that the new partner will be credited to the partnership. But in this scenario, the problem is silent as to the agreement of interest that M. Alice will be credited, in effect, the books will recognize M. Alice' interest equal to the cash she invested to the partnership.