Answer:

4.96%

Explanation:

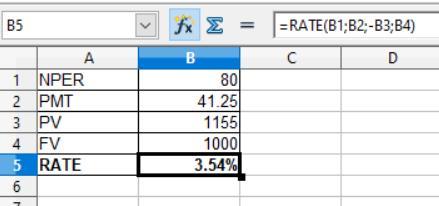

In order to determine the component after-tax cost of debt first we need to compute the before tax cost of debt by applying the RATE formula which is to be shown in the attachment below:

Given that,

Present value = $1,155

Future value or Face value = $1,000

PMT = 1,000 × 8.25% ÷ 2 = $41.25

NPER = 40 years × 2 = 80 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the above formula

1. The pretax cost of debt is 3.54% × 2 = 7.08%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 7.08% × ( 1 - 0.30)

= 4.96%

I believe that the strategy you are using when you only read the title, section headings, and captions is called the SQ3R reading method. The abbreviation stands for survey, question, read, recite, and review, and it helps you better understand your assignment.

Answer:

$11000

Explanation:

In general terms, assets held for sale are not depreciated, are measured at the lower of carrying amount and fair value fewer costs to selling, and are presented separately in the statement of financial position The company will report $11000 in 2x10 despite meeting criteria to be classified as held for sale, a loss is still elgibe to count down in the period in which it occurs. In this case, only one-month loss is counted.

Answer:

May's sales that are expected to be noncollectable are $7500.

Explanation:

The total collections from a months's credit sales is expected to be as follows,

35% in the month of sale

54% in the following month

6% in the second month after sale

The remaining is expected to be noncollectable.

The credit sales for a month are equal to 100%.

The percentage of noncollectable sales is = 100 - (35 + 54 + 6) = 5%

Thus, 5% of each month's sale is expected to be noncollectable.

May's sales that are expected to be noncollectable are,

Noncollectable Sales-May = 150000 * 0.05 = $7500