Answer:

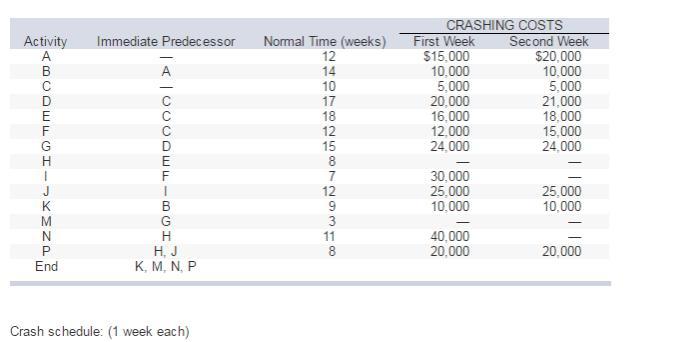

Hello your question has some missing data attached below is the missing data table

answer :

week 1 : C should be crashed at $5000

week 2 : C should be crashed at $5000

week 3 : F should be crashed at $12000

week 4 : F should be crashed at $15000

week 5 : P and E crashes at $20000 + $16000

Explanation:

Normal completion time = 49 weeks

and the critical path : ( C-F-I-J-P )

<u>Estimate the a minimum-cost crashing schedule</u>

At week 1 : the crash ( C )activity should be at $5000 and the completion time here will be 48 weeks

At week 2 : The crash (C ) activity should be made at $5000 hence the completion time here will be 47 weeks

At week 3 : The crash ( F ) activity should be made at $12000 and the completion time will be at 46 weeks

At week 4 : The crash ( F ) activity should be made at $15000 hence the completion time will be set at 45 weeks

At week 5 : The crash activity P will be at $20000 and crash activity E will be at $16000 hence the completion time will be 44 weeks

attached below is the pictorial view of the minimum-cost crashing schedule