<h2>Sebastian is employing <u>Goal setting</u> as a mechanism of career management.</h2>

Explanation:

<u>Goal setting:</u>

- Serve as a base for "Human resource Planning"

- It is proven that those employees who have goal setting will show good performance on their job.

- This will directly or indirectly promote the organization

- We can achieve organizational goals too

- Goal setting techniques are used by successful people around the world

- This might even be a favorite interview questions because the HR can understand how effective the employee would be for the organization.

The contract that carries the least risk for suppliers is CPPC. In this type of contract the buyer pays the supplier for allowable performance cost and pre-determined percentage based on total cost. The full meaning of CPPC is Cost Plus Percentage of Cost.

I believe the answer is:

1/Retirement plans

Especially the one that arranged by the government since it guaranteed by Federal banks

2/Property

The value would almost always increasing over time

3/A-rated bonds

A- rated bonds is score that given to the bond that have strong chance of return by credit rating company

4/Speculative stocks

If speculative stocks is scored by rating company, it would become B-rated or lower.

Answer:

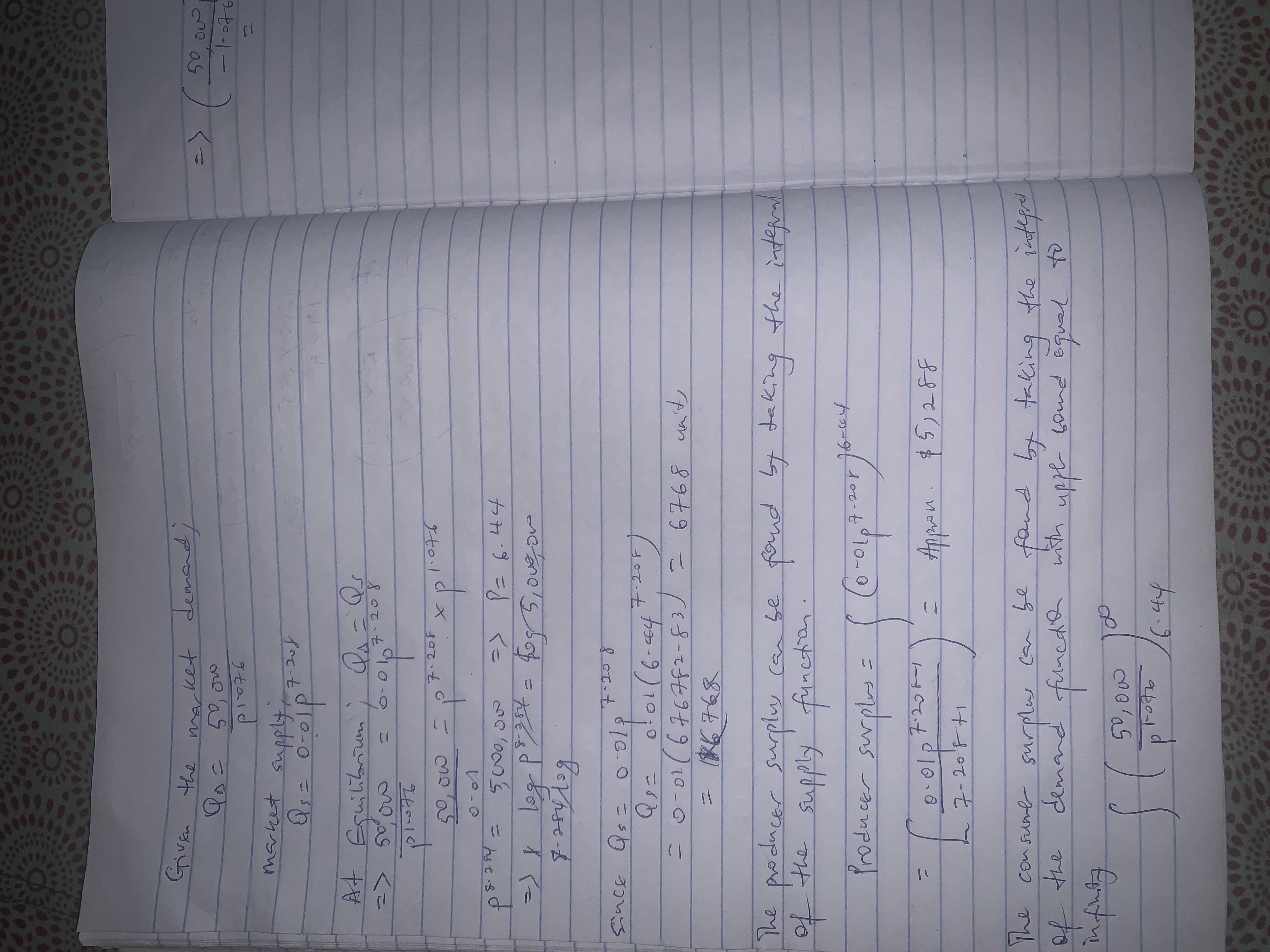

Equilibrium price and quantity

$6.44 and 6768

Consumer surplus

$571,081

Producer Surplus

$5,288

Explanation:

In this question, we are asked to calculate equilibrium price and quantity, consumer surplus and producer surplus.

Please check attachment for complete solution and step by step explanation