Answer:

Kindly check the attached images below for the well arranged account entries

Explanation:

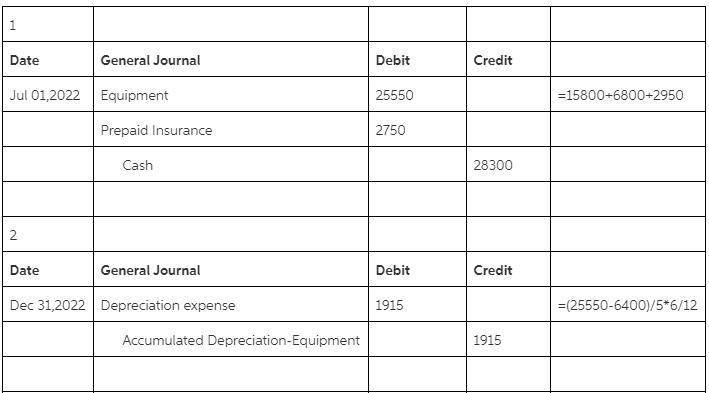

1

Date General Journal Debit Credit

Jul 01,2022 Equipment 25550 =15800+6800+2950

Prepaid Insurance 2750

Cash 28300

2

Date General Journal Debit Credit

Dec 31,2022 Depreciation expense 1915 =(25550-6400)/5*6/12

Accumulated Depreciation-Equipment 1915

3

Year Depreciation expense Accumulated

Depreciation Book value

2022 1915 1915 23635

2023 3830 5745 19805

2024 3830 9575 15975

2025 3830 13405 12145

2026 3830 17235 8315

2027 1915 19150 6400

Total 19150

4

Date General Journal Debit Credit

Dec 31,2022 Insurance expense 1375 =2750*6/12

Prepaid insurance 1375

Answer:

The correct answer is:

A. when employees at the acquired company willingly embrace the cultural values of the acquiring organization.

Explanation:

Normally, employees of a company are so used to their culture and work environment that for them the implementation of new strategies work is a great impact process. Although the workers accept the change in a voluntary basis, for new organizations it is necessary to apply a plan in order to help employees to meet and get familiar with the new environment and way of working. It is this process of change and progress that is known as deculturation, or implementation and change of different ideas and plans for the working place.

Answer:

2.85

Explanation:

U.S. Treasury bills are a risk-free asset, and thus have a beta of zero. Since Stock A has a risk-level equivalent to that of the overall market, its beta is one. Therefore, the beta for Stock B can be found by:

The beta of Stock B is 2.85.

Answer:

option (d) $500

Explanation:

Data provided in the question:

Reynolds Construction's value of operations = $750 million

short-term investments = $50 million

accounts payable = $100 million

notes payable = $100 million

long-term debt = $200 million

common stock = $40 million

retained earnings = $160 million

Now,

Firm value of equity

= Free cash flow value + Investments - Debt - Notes payable

= $750 million + $50 million - $200 million - $100 million

= $500 million

Hence,

the correct answer is option (d) $500