Answer: A) Fair value of the asset(s) given up.

Explanation:

Non-monetary exchange occurs when non-financial assets are exchanged in a transaction. Recording this transaction is based on the fair value of the assets exchanged and the recording is usually done in one of 3 ways being,

1. At the fair value of the asset transferred in exchange for it with a gain or loss on the exchange being recorded.

2. At the fair value of the asset received, if the fair value of this asset is more evident than the fair value of the asset transferred in exchange for it.

3. At the recorded amount of the surrendered asset, if no fair values are determinable or the transaction has no commercial substance.

If you need any clarification do comment.

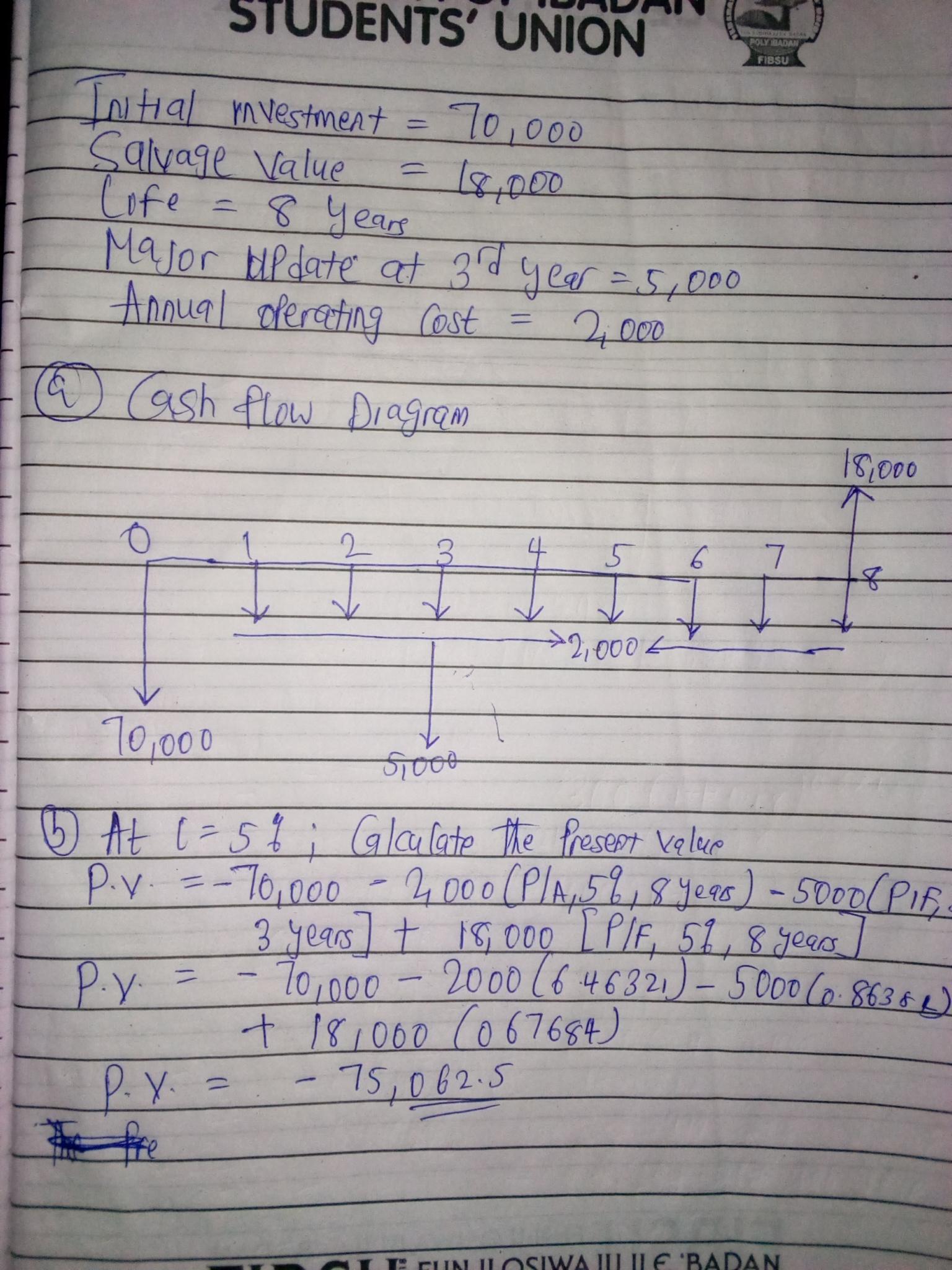

Answer:

The present value the expected costs of the new security and data management system is $-75,062.5

Explanation:

Kindly check attached picture for explanation

Answer:

<u>B</u>

<h3>Explanation:</h3>

Usually a life insurance policy stipulates that when th insured dies, the beneficiaries can file a claim to receive the life insurance money called the face value.

This face value is determine by certain factors like age, total coverage, medical history, gender, lifestyle, and job of the insured.

Answer:

Adhocracy Culture

Explanation:

An adhocracy culture is based on energy and creativity. Employees are encouraged to take risks, and leaders are seen as innovators or entrepreneurs. The organization is held together by experimentation, with an emphasis on individual ingenuity and freedom. The core values are based on change and agility.

Answer:

Variable Overhead Rate Variance $

Variable Overhead Efficiency Variance $

Variable Overhead Spending Variance $

Explanation:

Variable overhead rate variance = actual variable overhead - (actual direct hours x standard rate) = $9,510 - (16,200 x $0.80) = $9,510 - $12,960 = -$3,450 Favorable

Variable overhead efficiency variance = (actual labor hours - standard hours) x standard rate = (16,200 - 15,120) x $0.80 = 864 Unfavorable

Variable overhead spending variance = actual hours x (actual rate - standard rate) = 16,200 x ($0.59 - $0.80) = 16,200 x (-$0.21) = -$3,402 Favorable