I don't think there's anything more annoying than the ISP monopolies, specifically Comcast which has most of the US I believe. They never bother to upgrade their services only their prices and stupid cable bundle packages. I'm lucky enough to live in a large metropolitan area where a new fiber internet company just started up but before this last year there were only two ISP choices; Comcast or Century link. Suburban and rural areas typically only get one choice; expensive slow internet service from a local ISP monopoly.

Answer:

The correct answer is Variable Cost.

Explanation:

According to the scenario, the rent and manager salary is fixed, so, it is under fixed cost.

Whereas, Cost of supplies ( i.e. napkins, bags and condiments) are variable according to the number of customer. As the number of customer increases, cost of supply also increases and as the number of customer decreases, cost of supply also decreases.

This type of cost is known as Variable cost,

Hence, The cost of supply is Variable cost in the given scenario.

N/A which means Not applicable, due to the fact he has not yet been to college.

Answer:

Explanation:

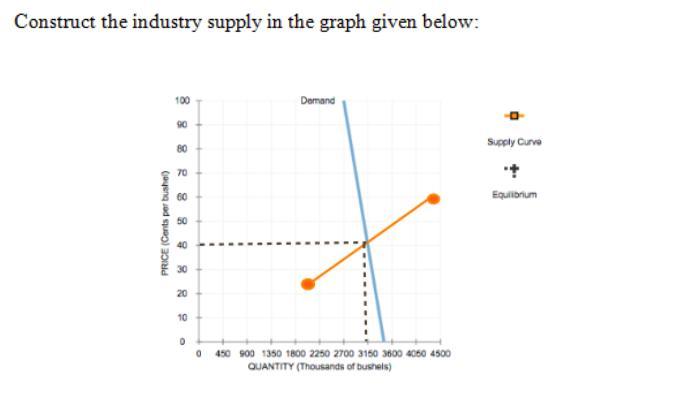

Suppose there is one perfect competitive market for wheat There are 90 firms in that industry.

Consider the Table 1 given below:

Table 1: Industry supply

MC individual Quantity (9) Industry quantity (Q)

25 30 30*90=2,700

40 35 35*90=3,150

55 40 40*90=3,600

70 45 45*90=4,050

Take possible MC (Marginal cost) with their respective individual. Calculate the industry supply by multiplying 90 with the firm's individual quantities as shown in Table 1 above.

Going by the graphical diagram in the attached image below, we can derive that:

The orange line represents the industry supply. The lower and higher orange represents the lowest and highest quantity respectively.

The intersection industry demand and industry supply gives the short run price and quantity

Therefor, the short run price and quantity are $40 and $3,150 respectively. This and can be shown with dotted black line.

So Therefore

At the current short run market price, the firms will produce in short run because this price is above the average variable cost

In the long, some firms will exit the market, given the current market price.

Answer and Explanation:

The English auction is a unique process of selling items, under which the auction starts at a low price and goes up to the maximum price and the item is sold to the highest bidder.

In this situation, Judi makes the highest bid which is worth $1,800, therefore, the cabinet will be sold to Judi at price $1,800 .