Answer:

It is cheaper to buy the seats.

Explanation:

Giving the following information:

The company is currently operating at 100% capacity, and variable manufacturing overhead is charged to production at the rate of 60% of direct labor cost. The direct materials and direct labor cost per unit to make the bicycle seats are $8.00 and $9.00, respectively. Normal production is 50,000 bicycles per year. A supplier offers to make the bicycle seats for $21 each. If the bicycle company accepts this offer, all variable manufacturing costs will be eliminated, but the $30,000 of fixed manufacturing overhead currently being charged to the bicycle seats will have to be absorbed by other products.

Make in house= [8 + 9 + (9*0.6)]*50,000= $1,120,000

Buy= 21*50,000= $1,050,000

It is cheaper to buy the seats.

Jello!!!l!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

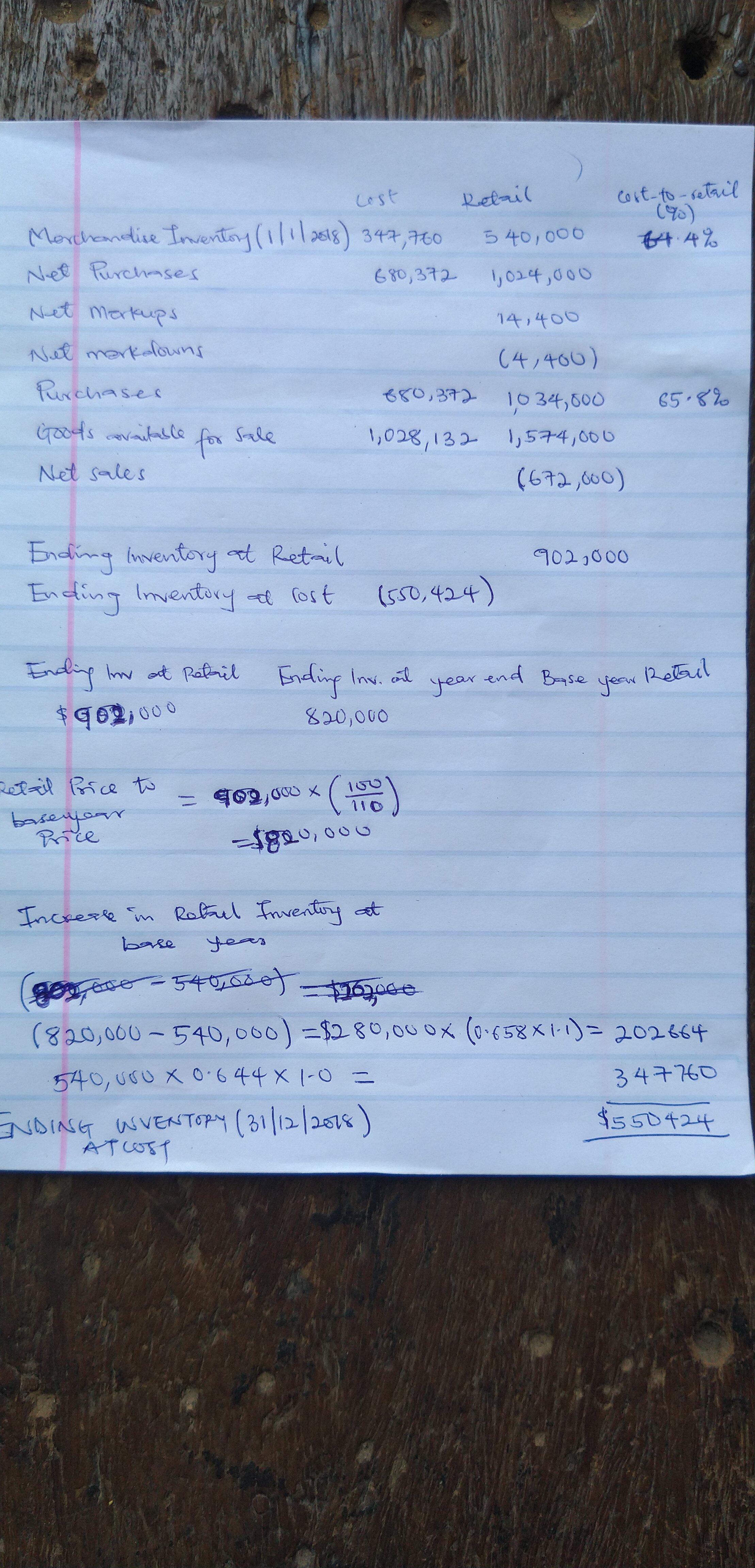

Answer:

Ending inventory at retail = $902,000

Ending inventory at cost = $550,424

Explanation:

Kindly check attached picture

Answer:

$1,275,000

Explanation:

The computation of the contribution margin is shown below:

As we know that

Contribution margin = Sales - variable cost

or

Selling price per unit - variable cost per unit

And, the direct material per unit, direct labor per unit, and the Variable overhead per unit are variable cost

So, if 50,000 units are sold, the contribution margin per unit is

= 50,000 × ($33 - $1.50 - $2.50 - $3.50)

= $1,275,000

I looked up the question, since this one is incomplete. I've attached an image of the correct chart. Elvis' marginal benefit of the fourth sandwich is his total benefit of eating 4 sandwich minus his total benefit from eating 3 sandwiches.

Looking at the chart, we see that this gives us 81-75 = 6.

Therefore, the Marginal Benefit of a fourth sandwich is 6.