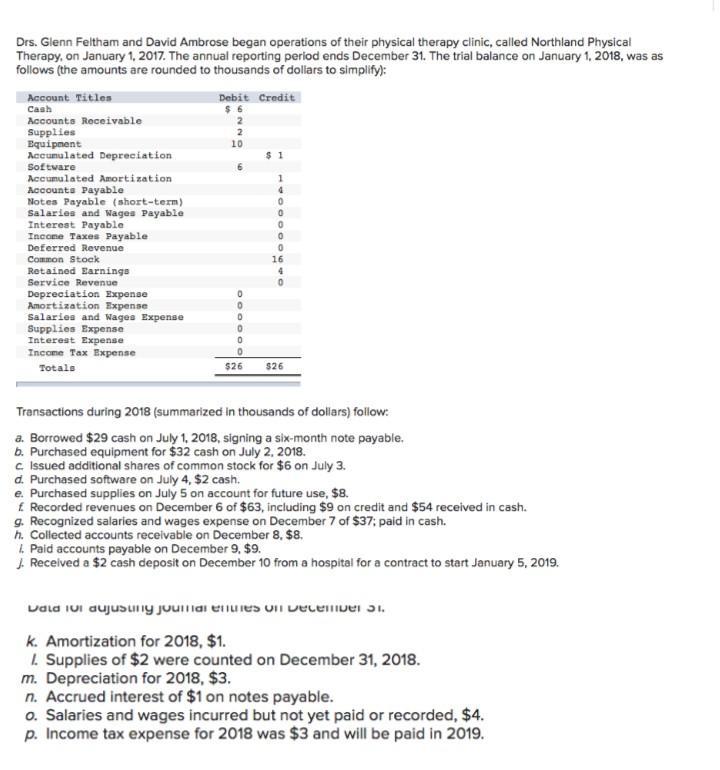

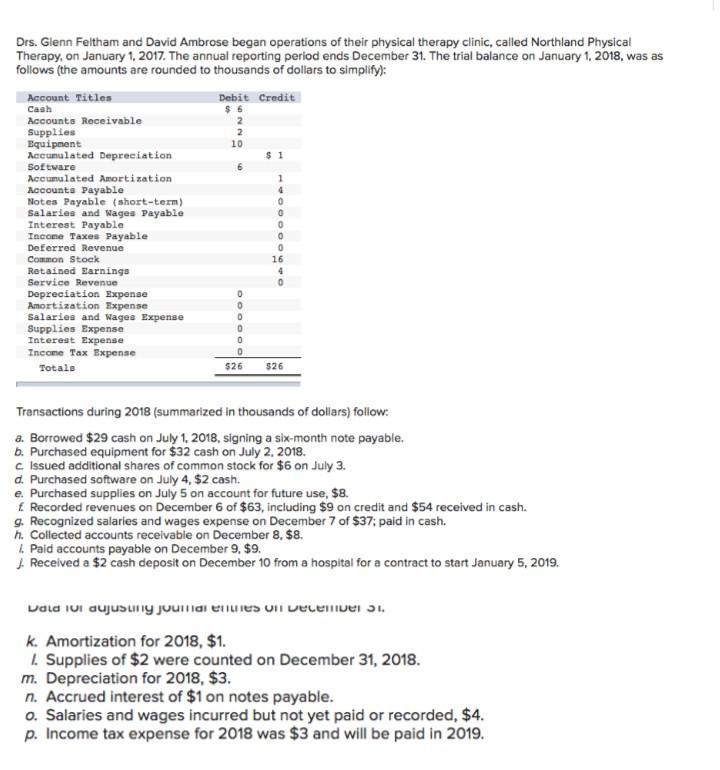

nuary 1, 2017. The annual reporting period ends December 31. The trial balance on January 1, 2018, was as follows (the amounts are rounded to thousands of dollars to simplify):

Account Titles Debit Credit

Cash $ 6

Accounts Receivable 2

Supplies 2

Equipment 10

Accumulated Depreciation $3

Software 8

Accumulated Amortization 3

Accounts Payable 6

Notes Payable (short-term) 0

Salaries and Wages Payable 0

Interest Payable 0

Income Taxes Payable 0

Deferred Revenue 0

Common Stock 13

Retained Earnings 3

Service Revenue 0

Depreciation Expense 0

Amortization Expense 0

Salaries and Wages Expense 0

Supplies Expense 0

Interest Expense 0

Income Tax Expense 0

Totals $28 $28

Transactions during 2018 (summarized in thousands of dollars) follow:

Borrowed $13 cash on July 1, 2018, signing a six-month note payable.

Purchased equipment for $16 cash on July 2, 2018.

Issued additional shares of common stock for $6 on July 3.

Purchased software on July 4, $2 cash.

Purchased supplies on July 5 on account for future use, $8.

Recorded revenues on December 6 of $47, including $9 on credit and $38 received in cash.

Recognized salaries and wages expense on December 7 of $21; paid in cash.

Collected accounts receivable on December 8, $8.

Paid accounts payable on December 9, $9.

Received a $2 cash deposit on December 10 from a hospital for a contract to start January 5, 2019.

Data for adjusting journal entries on December 31:

Amortization for 2018, $3.

Supplies of $2 were counted on December 31, 2018.

Depreciation for 2018, $3.

Accrued interest of $1 on notes payable.

Salaries and wages incurred but not yet paid or recorded, $4.

Income tax expense for 2018 was $3 and will be paid in 2019.

Record journal entries for transactions (a) through (j).

Cash 13

Notes-payable (short term) 13

Equipment 16

Cash 16

Cash 6

Common Stock 6

Software 2

Cash 2

Supplies 8

Accounts Payable 8

Accounts Receivable 9

Cash 38

Service Revenue 47

Salaries and Wages Expense 21

Cash 21

Cash 8

Accounts Receivable 8

Accounts Payable 9

Cash 9

Cash 2

Deferred Revenue 2

Set up T-accounts for the accounts on the trial balance. Enter beginning balances and post the transactions (a)-(j), adjusting entries (k)-(p), and closing entry.

Prepare an unadjusted trial balance and a trial balance.