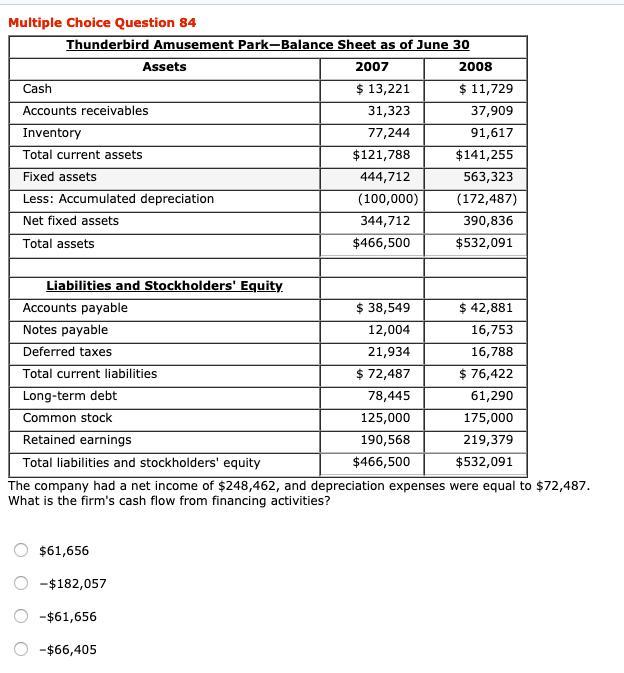

Complete Question:

The complete question can be seen the in the attachment at the end of the solution of the question.

Answer:

Option B. -$182,057

Explanation:

The Cash flow from financing activities can be calculated by using the following formula:

Cash flow from financing activities = Changes in the equity finance

+ Changes in long term borrowings + Changes in short term borrowings

- Interest paid - Dividends paid

Here

Changes in the equity = $175,000 common stock in year 2008

- $125,000 common stock in year 2008 = $50,000

Changes in long term Borrowings = $61,290 - $78,445 = - $17,155

Changes in short term Borrowings = $16,753 - $12,004 = $4749

Interest paid is $0 because interest rate is not given hence we can't calculate it.

Dividends paid = $190,568 Opening Retained Earnings + $248,462 Net Profit for the year - $219,379 Closing Retained Earnings = $219,651

Now, by putting values in the above equations, we have:

Cash flow from financing activities = $50,000 - $17,155 + $4749 - 0 - $219,651 = -$182,057