The answer should be software programming

I hope this helps you!!!

Answer:

False

Explanation:

The company either provides a service to its clients and sell its goods to the customers so that it can accomplish their targets and can achieve a maximum share in the market

In the given situation, it is mentioned that the company either performed a service, sells inventory i.e purchase from others but this is a wrong statement as it provides a service and sells its goods but not perform a service

Hence, the given statement is false

Answer:

The book value of the machine at the end of 2021 is $620000.

Explanation:

The straight line depreciation allocates a constant depreciation expense throughout the useful life of the machine. The straight line depreciation expense can be calculated using the following formula,

Depreciation expense per year = (Cost - Residual value) / estimated useful life

Depreciation expense per year = (1000000 - 50000) / 5 = $190000 per year

The book value of asset is the value of the asset calculated by deducting Accumulated depreciation from its cost.

The book value of the machine at the end of 2021 will be the, considering the depreciation expense for year 2021 has been charged,

Accumulated depreciation till 2021 end = 190000 for Year 2020 + 190000 for Year 2021 = $380000

Book value at the end of 2021 = 1000000 - 380000 = $620000

I think the answer is a but I am not for sure

Answer:

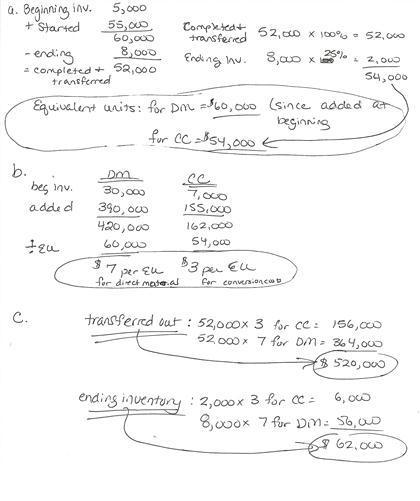

Answer for the question is given in the attachment.

Explanation: