Answer:

Nexium & Associates Journal entries

March 1

Dr Accounts Receivable800

Cr Service Revenue 800

March 9

Dr Office Furniture1,060

Cr Office Supplies 160

Cr Accounts Payable1,220

March 15

Dr Accounts Payable1,220

Cr Cash1,220

March 23

Dr Electricity Expense430

Cr Accounts Payable430

March 31

Dr Salaries Expense850

Cr Cash850

Explanation:

The details given about Nexium & Associates are straight forward and required no further

adjustment.

Answer:

Price lowers and becomes negative or -5.37 dollars

Explanation:

Market risk premium's formula could be written as dividends/price + dividend's growth rate. Therefore, we dividend growth rate according to the current price and dividend level equal to market risk premium - dividends/price or 0.15 - 1/15.43 = 0.086 or 8.6%. If the dividend growth rate rises by 25% than new one is 33.6%. Price is equal to dividends/market risk premium - dividend growth rate or in this case 1/0.15-0.336 or 1/-0.186 or -5.37 dollars. If the price is negative that would mean that any future selling of the stock would mean that ABC would have to pay in order to sell it.

Answer:

50% share.

Explanation:

Given:

There are only three firms in a market.

The largest firm has sales of $500 million.

The second-largest has sales of $300 million.

The smallest has sales of $200 million.

Question asked:

The market share of the largest firm is ?

Solution:

As we know:

Total sales of the largest company = $500 million.

Total sales of the market = Sales of largest firm + Sales of second largest firm+ Sales of smallest firm

Total sales of the market = $500 million + $300 million + $200 million

= $1000 million

Therefore, the market share of the largest firm is 50%.

Explanation:

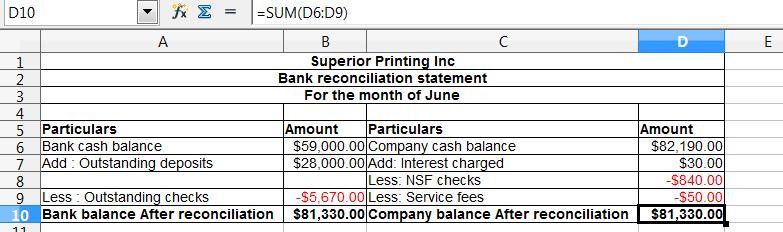

Bank Reconciliation: The Bank reconciliation deals with the balance of the bank statement and the balance of the cash statement. The aim is to compare those two statements to allow the organization to run smoothly.

There are various transactions because of which the balance of the bank statement and the balance of the cash statement do not match We change the transactions accordingly to match those statements

The preparation of the bank reconciliation statement for the month of June is presented in the spreadsheet. Kindly find the attachment below:

The outstanding checks is

= $770 + $4,600

= $5,670